# Google Colabで実行する場合は以下を実行しておく。

# !pip uninstall -y torch notebook notebook_shim tensorflow tensorflow-datasets prophet torchaudio torchdata torchtext torchvision

# インストールされていない場合には、以下を生かす。

# !pip install -U neuralprophet

# !pip install -U vega_datasets

# !pip install -U ipywidgetsNeuralProphetによる時系列データの予測

需要予測パッケージ NeuralProphet を紹介する.

NeuralProphetとは

NeuralProphet は需要予測のためのパッケージである.

Bayes推論に基づく予測パッケージ prophet と機械(深層)学習の橋渡しのために新たに開発されたもので、深層学習パッケージ PyTorch を用いている。

vega_datasetsのデータを用いるので,インストールしておく.

諸パッケージのインポート

NeuralProphetで予測するために必要なパッケージをインポートしておく.

import pandas as pd

from neuralprophet import NeuralProphet, set_log_level

# エラー以外はログメッセージを抑制

set_log_level("ERROR")

from vega_datasets import data

import plotly.express as px

import plotlyNeuralProphetの基本

NeuralProphetをPythonから呼び出して使う方法は,機械学習パッケージscikit-learnと同じである。

- NeuralProphetクラスのインスタンスmodelを生成

- fitメソッドで学習(引数はデータフレーム、返値は評価尺度)

- predictメソッドで予測(引数は予測したい期間を含んだデータフレーム)

例題:Wikiアクセス数

例としてアメリカンフットボールプレーヤのPayton ManningのWikiアクセス数のデータを用いる。

df = pd.read_csv("http://logopt.com/data/peyton_manning.csv")

df.head()| ds | y | |

|---|---|---|

| 0 | 2007-12-10 | 9.590761 |

| 1 | 2007-12-11 | 8.519590 |

| 2 | 2007-12-12 | 8.183677 |

| 3 | 2007-12-13 | 8.072467 |

| 4 | 2007-12-14 | 7.893572 |

Prophetモデルのインスタンスを生成し,fitメソッドで学習(パラメータの最適化)を行う.fitメソッドに渡すのは,上で作成したデータフレームである.このとき、ds(datestamp)列に日付(時刻)を、y列に予測したい数値を入れておく必要がある (この例題では,あらかじめそのように変更されている).

model = NeuralProphet()

metrics = model.fit(df)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

make_future_dataframeメソッドで未来の時刻を表すデータフレームを生成する。 既定値では予測で用いた過去の時刻も含まないので、n_historic_predictions引数をTrueにして、過去の時刻も入れる。 引数は予測をしたい期間数periodsであり,ここでは、1年後(365日分)まで予測することにする。

df_future = model.make_future_dataframe(df, n_historic_predictions=True, periods=365)

forecast = model.predict(df_future)

model.set_plotting_backend("matplotlib") #matplotlibで描画する(既定値はplotly)

model.plot(forecast)

predict メソッドに予測したい時刻を含んだデータフレームfuture を渡すと、予測値を入れたデータフレームforecastを返す。

forecast.tail()| ds | y | yhat1 | trend | season_yearly | season_weekly | |

|---|---|---|---|---|---|---|

| 3265 | 2017-01-15 | NaN | 8.216602 | 7.137280 | 1.036658 | 0.042665 |

| 3266 | 2017-01-16 | NaN | 8.550267 | 7.136175 | 1.049828 | 0.364264 |

| 3267 | 2017-01-17 | NaN | 8.316690 | 7.135070 | 1.060175 | 0.121446 |

| 3268 | 2017-01-18 | NaN | 8.133187 | 7.133965 | 1.067564 | -0.068342 |

| 3269 | 2017-01-19 | NaN | 8.133450 | 7.132861 | 1.071885 | -0.071296 |

一般化加法モデル

NeuralProphetにおける予測は一般化加法モデルを用いて行われる. これは,傾向変動,季節変動,イベント情報などの様々な因子の和として予測を行う方法である.

\[ y_t =g_t + s_t + h_t + f_t + a_t + \ell_t + \epsilon_t \]

- \(y_t\) : 予測値

- \(g_t\) : 傾向変動(trend);傾向変化点ありの区分的線形(アフィン)関数

- \(s_t\) : 季節変動;年次,週次,日次の季節変動をsin, cosの組み合わせ(フーリエ級数)で表現

- \(h_t\) : 休日などのイベント項

- \(f_t\): 外生変数に対する回帰項

- \(a_t\): 自己回帰項(時間遅れ(ラグ)を指定する)

- \(\ell_t\): 時間遅れ(ラグ)付きの外生変数に対する回帰項

- \(\epsilon_t\) : 誤差項

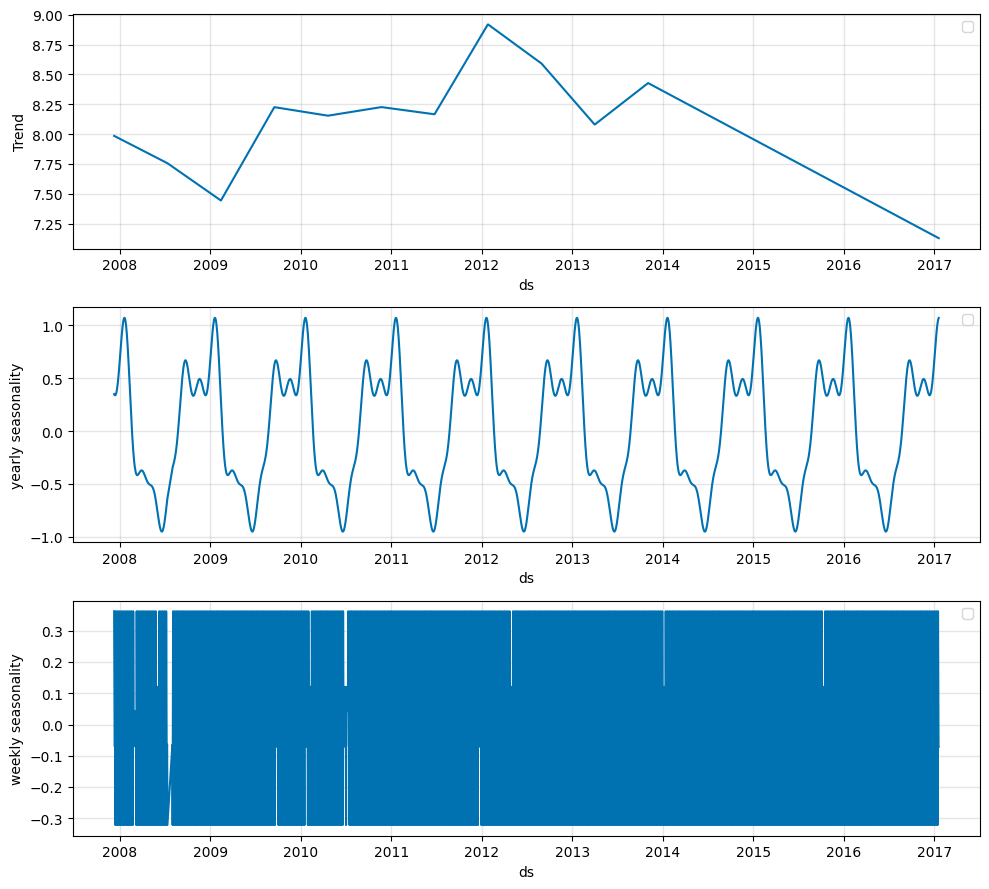

因子ごとに予測値の描画を行うには,plot_componentsメソッドを用いる.既定では,以下のように,上から順に傾向変動,年次の季節変動、週次の季節変動が描画される.また,傾向変動の図(一番上)には,予測の誤差範囲が示される.季節変動の誤差範囲を得る方法については,後述する.

model.plot_components(forecast)

対話形式に,拡大縮小や範囲指定ができる動的な図も,Plotlyライブラリを用いて得ることができる.

model.set_plotting_backend("plotly")

fig = model.plot(forecast)

#plotly.offline.plot(fig);

例題: \(CO_2\) 排出量のデータ

データライブラリから二酸化炭素排出量のデータを読み込み,Plotly Expressで描画する.

co2 = data.co2_concentration()

co2.head()| Date | CO2 | |

|---|---|---|

| 0 | 1958-03-01 | 315.70 |

| 1 | 1958-04-01 | 317.46 |

| 2 | 1958-05-01 | 317.51 |

| 3 | 1958-07-01 | 315.86 |

| 4 | 1958-08-01 | 314.93 |

fig = px.line(co2,x="Date",y="CO2")

#plotly.offline.plot(fig);

列名の変更には,データフレームのrenameメソッドを用いる.引数はcolumnsで,元の列名をキーとし,変更後の列名を値とした辞書を与える.また,元のデータフレームに上書きするために,inplace引数をTrueに設定しておく.

co2.rename(columns={"Date":"ds","CO2":"y"},inplace=True)

co2.head()| ds | y | |

|---|---|---|

| 0 | 1958-03-01 | 315.70 |

| 1 | 1958-04-01 | 317.46 |

| 2 | 1958-05-01 | 317.51 |

| 3 | 1958-07-01 | 315.86 |

| 4 | 1958-08-01 | 314.93 |

make_future_dataframeメソッドで未来の時刻を表すデータフレームを生成する。既定値では、(予測で用いた)過去の時刻も含む。 ここでは、200ヶ月先まで予測することにする。

そのために,引数 periods を200に設定しておく

predict メソッドに予測したい時刻を含んだデータフレームfuture を渡すと、予測値を入れたデータフレームforecastを返す。

最後にplotメソッドで表示する.

model = NeuralProphet()

metrics = model.fit(co2)

future = model.make_future_dataframe(co2, n_historic_predictions=True, periods=200)

forecast = model.predict(future)

model.set_plotting_backend("plotly")

model.plot(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

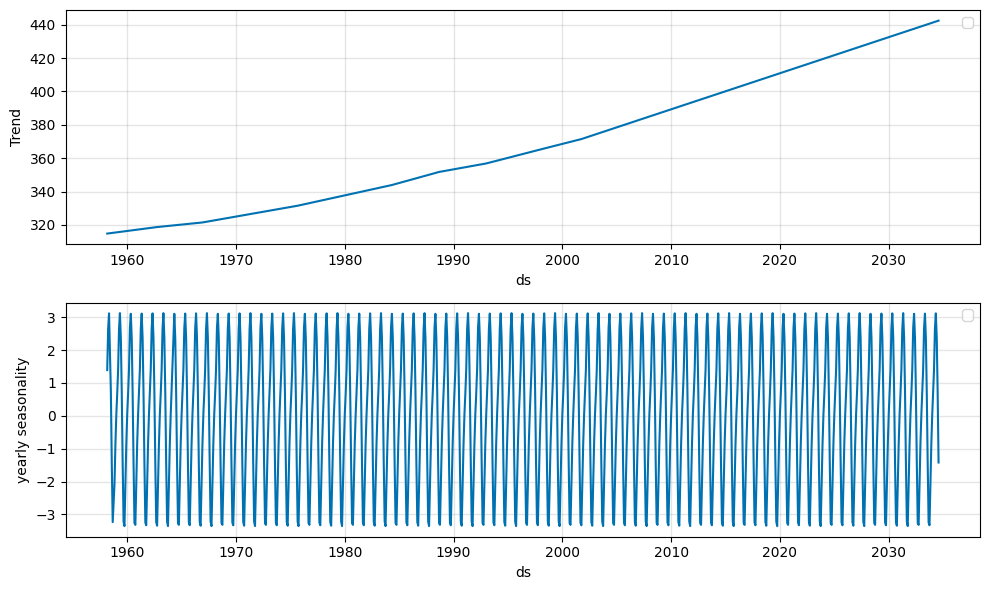

予測は一般化加法モデルを用いて行われる.

これは,傾向変動,季節変動,イベント情報などの様々な因子の和として予測を行う方法である.

上に表示されているように,週次と日次の季節変動は無視され,年次の季節変動のみ考慮して予測している.

因子ごとに予測値の描画を行うには,plot_componentsメソッドを用いる.既定では,以下のように,上から順に傾向変動,年次の季節変動が描画される.

model.plot_components(forecast)

例題:航空機乗客数のデータ

Prophetの既定値では季節変動は加法的モデルであるが、問題によっては乗法的季節変動の方が良い場合もある。 例として、航空機の乗客数を予測してみよう。最初に既定値の加法的季節変動モデルで予測し,次いで乗法的モデルで予測する.

passengers = pd.read_csv("http://logopt.com/data/AirPassengers.csv")

passengers.head()| Month | #Passengers | |

|---|---|---|

| 0 | 1949-01 | 112 |

| 1 | 1949-02 | 118 |

| 2 | 1949-03 | 132 |

| 3 | 1949-04 | 129 |

| 4 | 1949-05 | 121 |

fig = px.line(passengers,x="Month",y="#Passengers")

#plotly.offline.plot(fig);

passengers.rename(inplace=True,columns={"Month":"ds","#Passengers":"y"})

passengers.head()| ds | y | |

|---|---|---|

| 0 | 1949-01 | 112 |

| 1 | 1949-02 | 118 |

| 2 | 1949-03 | 132 |

| 3 | 1949-04 | 129 |

| 4 | 1949-05 | 121 |

季節変動を乗法的に変更するには, モデルの seasonality_mode 引数を乗法的を表す multiplicative に設定する.

また、モデルを作成するときに、引数quantilesで不確実性の幅を表示するようにする。以下では、5%と95%の幅を表示させている。

model = NeuralProphet(quantiles=[0.05, 0.95])

metrics = model.fit(passengers)

future = model.make_future_dataframe(passengers, periods=20, n_historic_predictions=True)

forecast = model.predict(future)

model.set_plotting_backend("plotly")

model.plot(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

model = NeuralProphet(quantiles=[0.05, 0.95], seasonality_mode="multiplicative")

metrics = model.fit(passengers)

future = model.make_future_dataframe(passengers, periods=20, n_historic_predictions=True)

forecast = model.predict(future)

model.set_plotting_backend("plotly")

model.plot(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

結果から,乗法的季節変動の方が,良い予測になっていることが確認できる.

問題(小売りの需要データ)

以下の,小売りの需要データを描画し,予測を行え. ただし,モデルは乗法的季節変動で,月次で予測せよ.

retail = pd.read_csv(`http://logopt.com/data/retail_sales.csv`)

retail.head()| ds | y | |

|---|---|---|

| 0 | 1992-01-01 | 146376 |

| 1 | 1992-02-01 | 147079 |

| 2 | 1992-03-01 | 159336 |

| 3 | 1992-04-01 | 163669 |

| 4 | 1992-05-01 | 170068 |

例題: 1時間ごとの気温データ

ここではシアトルの気温の予測を行う.

climate = data.seattle_temps()

climate.head()| date | temp | |

|---|---|---|

| 0 | 2010-01-01 00:00:00 | 39.4 |

| 1 | 2010-01-01 01:00:00 | 39.2 |

| 2 | 2010-01-01 02:00:00 | 39.0 |

| 3 | 2010-01-01 03:00:00 | 38.9 |

| 4 | 2010-01-01 04:00:00 | 38.8 |

このデータは, date 列に日付と1時間ごとの時刻が, temp 列に気温データが入っている.

NeuralProphetは, 日別でないデータも扱うことができる。 date列のデータ形式は、日付を表すYYYY-MM-DDの後に時刻を表すHH:MM:SSが追加されている。 未来の時刻を表すデータフレームは、make_future_dataframeメソッドで生成する。

climate["Date"] = pd.to_datetime(climate.date)climate.rename(columns={"Date":"ds","temp":"y"},inplace=True)climate = climate[["ds","y"]] #余分な列を削除するmodel = NeuralProphet(daily_seasonality=True)

metrics = model.fit(climate)

future = model.make_future_dataframe(climate, periods=200, n_historic_predictions=True)

forecast = model.predict(future)

model.set_plotting_backend("plotly")

model.plot(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

因子ごとに予測値を描画すると,傾向変動と週次の季節変動の他に,日次の季節変動(1日の気温の変化)も出力される.

model.plot_components(forecast)問題(サンフランシスコの気温データ)

以下のサンフランシスコの気温データを描画し,時間単位で予測を行え.

sf = data.sf_temps()

sf.head()| temp | date | |

|---|---|---|

| 0 | 47.8 | 2010-01-01 00:00:00 |

| 1 | 47.4 | 2010-01-01 01:00:00 |

| 2 | 46.9 | 2010-01-01 02:00:00 |

| 3 | 46.5 | 2010-01-01 03:00:00 |

| 4 | 46.0 | 2010-01-01 04:00:00 |

傾向変化点

「上昇トレンドの株価が,下降トレンドに移った」というニュースをよく耳にするだろう.このように,傾向変動は,時々変化すると仮定した方が自然なのだ.NeuralProphetでは,これを傾向変化点として処理する.再び,Peyton Manningのデータを使う.

傾向変化点の数はn_changepointsで指定する。既定値は \(10\) である。以下では、傾向変化点を \(5\) に設定する。

df = pd.read_csv("http://logopt.com/data/peyton_manning.csv")

model = NeuralProphet(n_changepoints=5)

model.fit(df)

future = model.make_future_dataframe(df, periods=365, n_historic_predictions=True)

forecast = model.predict(future)

model.plot(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning: MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

rank_zero_warn(

model.plot_components(forecast)傾向変化点のリストをchangepoints引数で与えることもできる。以下の例では、1つの日だけで変化するように設定している。

model = NeuralProphet(changepoints=["2014-01-01"])

model.fit(df)

future = model.make_future_dataframe(df, periods=365, n_historic_predictions=True)

forecast = model.predict(future)

model.plot(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

model.plot_components(forecast)例題 SP500データ

株価の予測を行う.

傾向変化点の候補は自動的に設定される。既定値では時系列の最初の80%の部分に均等に設定される。これは、モデルのchangepoint_range引数で設定する. この例では,期間の終わりで変化点を設定したいので,0.95に変更する.

年次の季節変動の変化の度合いは、yearly_seasonality(既定値は \(10\)) で制御できる。この例では,このパラメータを \(5\) に変更することによって年間の季節変動を抑制して予測を行う.

sp500 = data.sp500()

sp500.tail()| date | price | |

|---|---|---|

| 118 | 2009-11-01 | 1095.63 |

| 119 | 2009-12-01 | 1115.10 |

| 120 | 2010-01-01 | 1073.87 |

| 121 | 2010-02-01 | 1104.49 |

| 122 | 2010-03-01 | 1140.45 |

sp500.rename(inplace=True,columns={"date":"ds","price":"y"})model = NeuralProphet(changepoints_range=0.95, yearly_seasonality=5)

model.fit(sp500)

future = model.make_future_dataframe(sp500, periods=20, n_historic_predictions=True)

forecast = model.predict(future)

model.plot(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

model.plot_components(forecast)例題: 個別銘柄の株価の予測

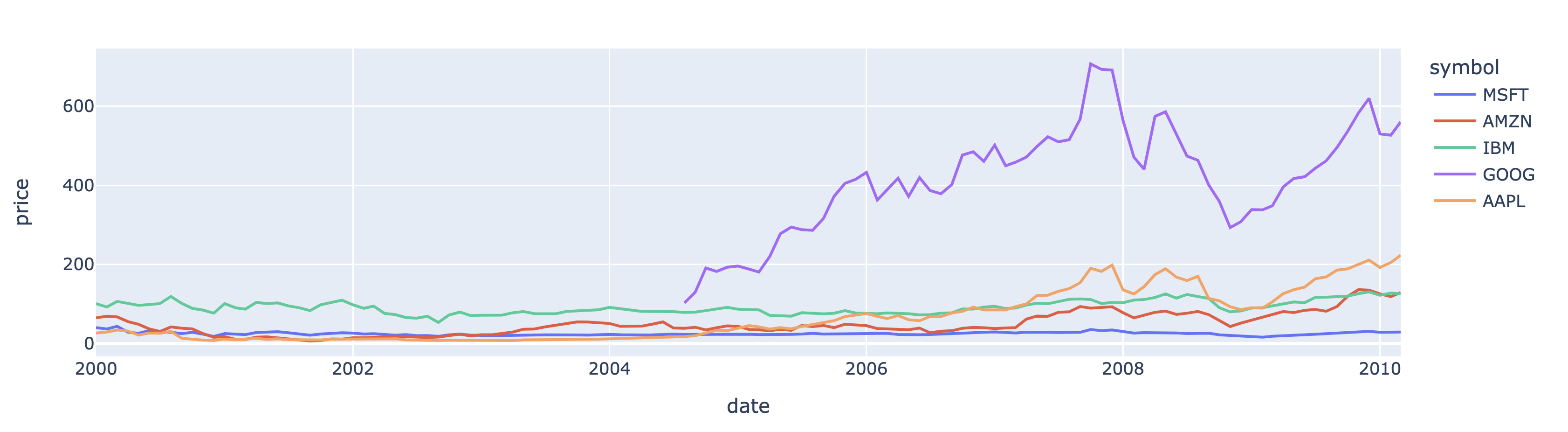

stocksデータでは,symbol列に企業コードが入っている.

- AAPL アップル

- AMZN アマゾン

- IBM IBM

- GOOG グーグル

- MSFT マイクロソフト

まずは可視化を行う。

stocks = data.stocks()

stocks.tail()| symbol | date | price | |

|---|---|---|---|

| 555 | AAPL | 2009-11-01 | 199.91 |

| 556 | AAPL | 2009-12-01 | 210.73 |

| 557 | AAPL | 2010-01-01 | 192.06 |

| 558 | AAPL | 2010-02-01 | 204.62 |

| 559 | AAPL | 2010-03-01 | 223.02 |

fig = px.line(stocks,x="date",y="price",color="symbol")

#plotly.offline.plot(fig);

以下では,マイクロソフトの株価を予測してみる.

msft = stocks[stocks.symbol == "MSFT"]

msft.head()| symbol | date | price | |

|---|---|---|---|

| 0 | MSFT | 2000-01-01 | 39.81 |

| 1 | MSFT | 2000-02-01 | 36.35 |

| 2 | MSFT | 2000-03-01 | 43.22 |

| 3 | MSFT | 2000-04-01 | 28.37 |

| 4 | MSFT | 2000-05-01 | 25.45 |

msft = msft.rename(columns={"date":"ds","price":"y"})

msft = msft[["ds","y"]]

msft.head()| ds | y | |

|---|---|---|

| 0 | 2000-01-01 | 39.81 |

| 1 | 2000-02-01 | 36.35 |

| 2 | 2000-03-01 | 43.22 |

| 3 | 2000-04-01 | 28.37 |

| 4 | 2000-05-01 | 25.45 |

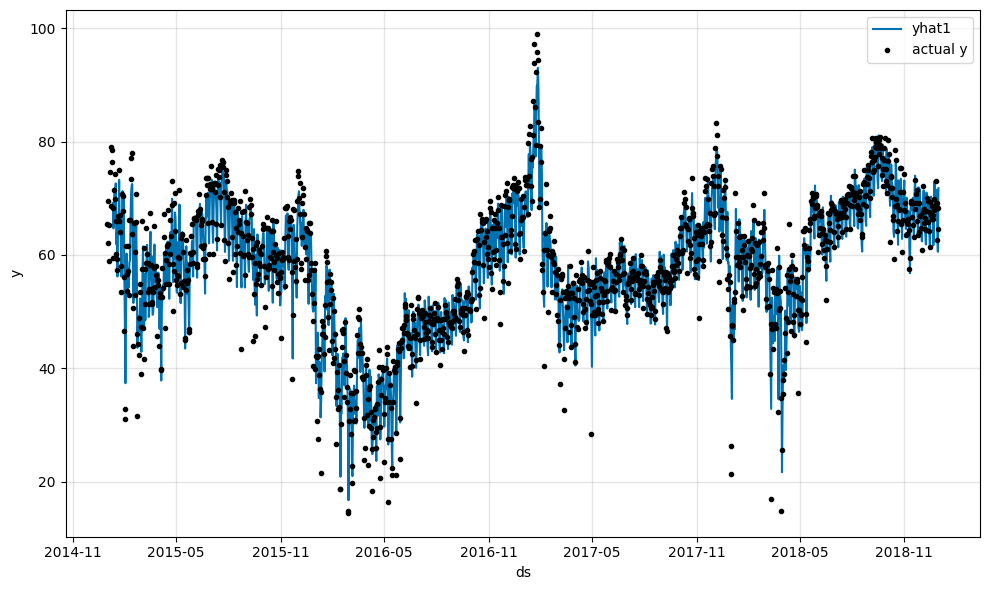

model = NeuralProphet(changepoints_range=0.95,yearly_seasonality=5)

model.fit(msft)

future = model.make_future_dataframe(msft, periods=20, n_historic_predictions=True)

forecast = model.predict(future)

model.plot(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

#model.plot_components(forecast)

model.plot_parameters(forecast)問題(株価)

上の株価データのマイクロソフト以外の銘柄を1つ選択し,予測を行え.

stocks = data.stocks()

stocks.head()| symbol | date | price | |

|---|---|---|---|

| 0 | MSFT | 2000-01-01 | 39.81 |

| 1 | MSFT | 2000-02-01 | 36.35 |

| 2 | MSFT | 2000-03-01 | 43.22 |

| 3 | MSFT | 2000-04-01 | 28.37 |

| 4 | MSFT | 2000-05-01 | 25.45 |

発展編

以下では,NeuralProphetの高度な使用法を解説する.

自己回帰による予測

以下の例は、スペインの4年間のエネルギー価格である。 直近の \(p\) 日前までのデータの重み付きの和の項を追加するのが、自己回帰モデルである。 \(p\) を表すn_legs引数を設定すると、自己回帰項が追加される。

df = pd.read_csv("https://github.com/ourownstory/neuralprophet-data/raw/main/kaggle-energy/datasets/tutorial01.csv")

df.head()| ds | y | |

|---|---|---|

| 0 | 2014-12-31 | 65.41 |

| 1 | 2015-01-01 | 62.09 |

| 2 | 2015-01-02 | 69.44 |

| 3 | 2015-01-03 | 65.22 |

| 4 | 2015-01-04 | 58.91 |

model = NeuralProphet(

yearly_seasonality=True,

weekly_seasonality=True,

daily_seasonality=True,

n_lags=10

)

model.set_plotting_backend("matplotlib")

metrics = model.fit(df)

forecast = model.predict(df)

model.plot(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

model.plot_parameters()

休日(特別なイベント)を考慮した予測

休日や特別なイベントをモデルに追加することを考える。

モデルインスタンスのadd_country_holidaysメソッドを用いて,各国(州)の休日データを追加することができる。 引数は python-holidays にある文字列で、 たとえば米国の場合にはUS、スペインの場合にはESを指定する。

df = pd.read_csv("https://github.com/ourownstory/neuralprophet-data/raw/main/kaggle-energy/datasets/tutorial01.csv")

df.head()| ds | y | |

|---|---|---|

| 0 | 2014-12-31 | 65.41 |

| 1 | 2015-01-01 | 62.09 |

| 2 | 2015-01-02 | 69.44 |

| 3 | 2015-01-03 | 65.22 |

| 4 | 2015-01-04 | 58.91 |

model = NeuralProphet()

model.set_plotting_backend("matplotlib")

model = model.add_country_holidays("US")

metrics = model.fit(df)

forecast = model.predict(df)

model.plot(forecast)

model.plot_components(forecast)

悪天候(extreme_weather)を表すデータフレームを与えることによって、特別なイベントを考慮した予測を行うことができる。 データフレームはeventとdsの列をもち、それをadd_eventsメソッドで追加する。 その後、create_df_with_eventsでイベントが追加されたデータフレームを生成する。

df_events = pd.DataFrame(

{

"event": "extreme_weather",

"ds": pd.to_datetime(

[

"2018-11-23",

"2018-11-17",

"2018-10-28",

"2018-10-18",

"2018-10-14",

]

),

}

)

df_events.head()| event | ds | |

|---|---|---|

| 0 | extreme_weather | 2018-11-23 |

| 1 | extreme_weather | 2018-11-17 |

| 2 | extreme_weather | 2018-10-28 |

| 3 | extreme_weather | 2018-10-18 |

| 4 | extreme_weather | 2018-10-14 |

model = NeuralProphet()

model.set_plotting_backend("matplotlib")

model.add_events("extreme_weather")

df_all = model.create_df_with_events(df, df_events)

df_all.head()| ds | y | extreme_weather | |

|---|---|---|---|

| 0 | 2014-12-31 | 65.41 | 0.0 |

| 1 | 2015-01-01 | 62.09 | 0.0 |

| 2 | 2015-01-02 | 69.44 | 0.0 |

| 3 | 2015-01-03 | 65.22 | 0.0 |

| 4 | 2015-01-04 | 58.91 | 0.0 |

metrics = model.fit(df_all)

forecast = model.predict(df_all)

model.plot(forecast)

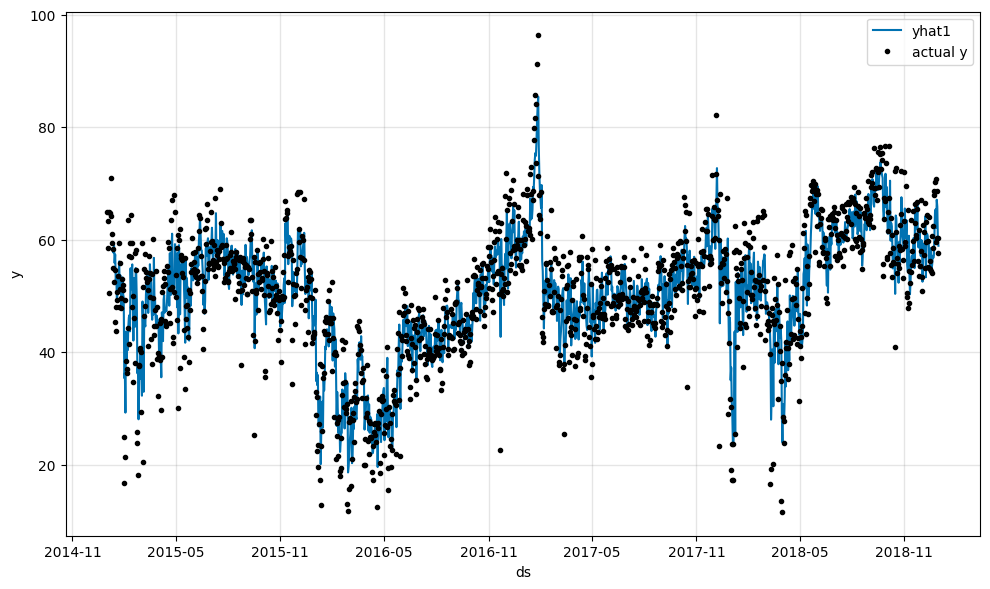

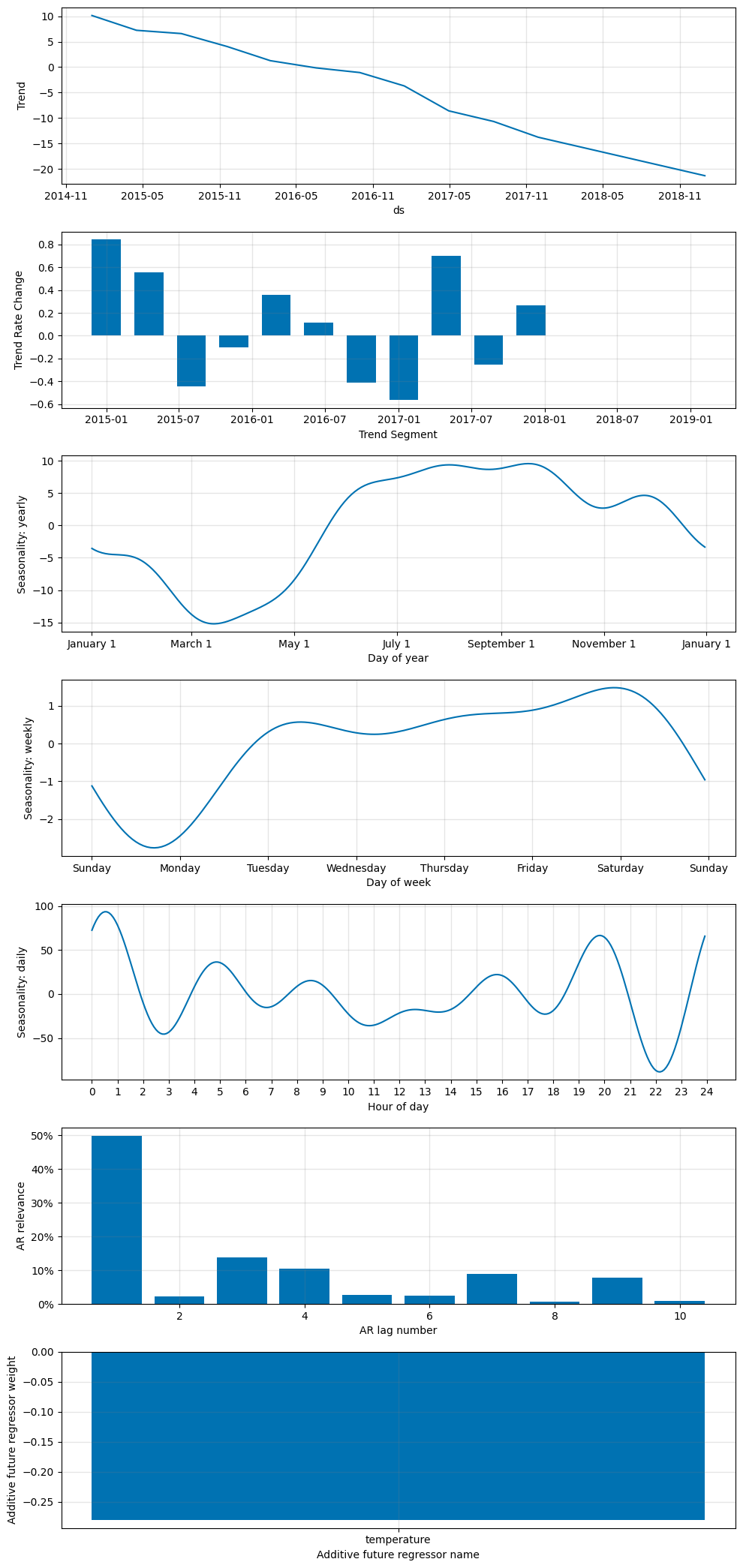

外生変数の追加

外生変数である気温temperatureを利用してエネルギー価格の予測を行う。

ここでは、\(q\) 日前までの気温がエネルギー価格に影響を与える時間遅れ(ラグ)モデルを用いる。 モデルインスタンスのaddd_lagged_regressorメソッドを用いる。 引数は列名もしくは列名のリストである。時間遅れのパラメータ \(q\) は引数n_lagsで与える。

また、未来の気温が既知であると仮定した場合には、気温を外生変数とした回帰項を追加する。 これには、モデルインスタンスの add_future_regressorを用いる。 引数は列名もしくは列名のリストである。

df = pd.read_csv("https://github.com/ourownstory/neuralprophet-data/raw/main/kaggle-energy/datasets/tutorial04.csv")

df.head()| ds | y | temperature | |

|---|---|---|---|

| 0 | 2015-01-01 | 64.92 | 277.00 |

| 1 | 2015-01-02 | 58.46 | 277.95 |

| 2 | 2015-01-03 | 63.35 | 278.83 |

| 3 | 2015-01-04 | 50.54 | 279.64 |

| 4 | 2015-01-05 | 64.89 | 279.05 |

model = NeuralProphet(

yearly_seasonality=True,

weekly_seasonality=True,

daily_seasonality=True,

n_lags=10

)

model.set_plotting_backend("matplotlib")

#model.add_lagged_regressor("temperature", n_lags=5)

model.add_future_regressor("temperature")

metrics = model.fit(df)

forecast = model.predict(df)

model.plot(forecast)

model.plot_parameters()

ユーザーが設定した季節変動

Prophetでは既定値の年次(yearly)や週次(weekly)や日次(daily)の季節変動だけでなく、ユーザー自身で季節変動を定義・追加できる。 以下では、週次の季節変動を除き,かわりに周期が30.5日の月次変動をフーリエ次数(seasonalityの別名)5として追加している。

df = pd.read_csv("http://logopt.com/data/peyton_manning.csv")

model = NeuralProphet(weekly_seasonality=False)

model.add_seasonality(name="monthly", period=30.5, fourier_order=5)

model.fit(df)

future = model.make_future_dataframe(df, n_historic_predictions=True, periods=365)

forecast = model.predict(future)

model.plot_components(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

他の要因に依存した季節変動

他の要因に依存した季節変動も定義・追加することができる。以下の例では、オンシーズンとオフシーズンごと週次変動を定義し、追加してみる。

df["ds"] = pd.to_datetime(df["ds"])

df["on_season"] = df["ds"].apply(lambda x: x.month in [9, 10, 11, 12, 1])

df["off_season"] = df["ds"].apply(lambda x: x.month not in [9, 10, 11, 12, 1])model = NeuralProphet(weekly_seasonality=False)

model.add_seasonality(name="weekly_on_season", period=7, fourier_order=3, condition_name="on_season")

model.add_seasonality(name="weekly_off_season", period=7, fourier_order=3, condition_name="off_season")

metrics = model.fit(df, freq="D")

future = model.make_future_dataframe(df, n_historic_predictions=True, periods=365)

forecast = model.predict(future)

model.plot_components(forecast)WARNING - (py.warnings._showwarnmsg) - /Users/mikiokubo/Library/Caches/pypoetry/virtualenvs/analytics2-0ZiTWol9-py3.9/lib/python3.9/site-packages/pytorch_lightning/trainer/setup.py:201: UserWarning:

MPS available but not used. Set `accelerator` and `devices` using `Trainer(accelerator='mps', devices=1)`.

主なパラメータと既定値

以下にNeuralProphetの主要なパラメータ(引数)とその既定値を示す.

- changepoints=None : 傾向変更点のリスト

- changepoint_range = \(0.8\) : 傾向変化点の候補の幅(先頭から何割を候補とするか)

- n_changepoints= \(10\) : 傾向変更点の数

- trend_reg = \(0\) : 傾向変動の正則化パラメータ

- yearly_seasonality=

auto: 年次の季節変動を考慮するか否か - weekly_seasonality=

auto: 週次の季節変動を考慮するか否か - daily_seasonality=

auto: 日次の季節変動を考慮するか否か - seasonality_mode =

additive: 季節変動が加法的(additive)か乗法的(multiplicative)か - seasonality_reg= \(0\) : 季節変動の正則化パラメータ

- n_forecasts = \(1\) : 予測数

- n_lags = \(0\): 時間ずれ(ラグ)

- ar_reg = \(0\): 自己回帰の正則化パラメータ

- quantile= \([]\) : 不確実性を表示するための分位数のリスト